18th June – 24th June 2018

Share:

- Date: 18/06/2018

Front and centre of our thoughts this week include

For football fans, the highlight of the week will be England’s opening world cup game against Tunisia. Whilst there may be theatrics on the pitch, the drama at Westminster is likely to continue. The EU Withdrawal Bill is set to return to the House of Lords before making its way back to the House of Commons for what looks like a fresh battle this week. Last week Theresa May’s government successfully defeated a number of amendments to the bill that would have complicated the Brexit process. However in order to do so, she had to make a number of compromises to Pro-EU members of her party. However, these members felt the agreed amendments were not reflected in the government's final draft. The extent to which Parliament will have a 'meaningful vote' if no deal is reached with the EU by 21 January 2019 is of particular importance to this group. As a result, a fresh battle looks likely to rage this week when the EU Withdrawal Bill heads back to the Commons. With both pro-EU and Brexiteers within the Conservative and Labour Party, it is extremely difficult to predict an outcome for this set of negotiations, other than the battle over the EU Withdrawal Bill looks far from over.

Staying with the UK, the Bank of England (BoE) holds a monetary policy meeting this week and is widely expected to make no change to interest rates. Incoming data continues to show that the UK economy is not firing on all cylinders. Consumer spending, employment and business confidence surveys have been fairly solid and supportive of growth, whilst industrial production and manufacturing have been exceptionally weak. The minutes of the meeting will be closely scrutinised to see whether policy members sit on the optimistic or pessimistic side of the fence in regards to recent data, with the tone of the minutes likely to set expectations over the possibility of an interest rate rise in August.

Elsewhere, the annual ECB Forum on Central Banking, takes place in Sintra, Portugal this week. The meeting brings central bank governors, academics and high-level financial market representatives to exchange views on current policy issues with the theme of this year’s meeting being "Price and wage setting in advanced economies". With the European Central Bank (ECB), US Federal Reserve (Fed) and the Bank of Japan (BoJ) all holding monetary policy meetings last week it is unlikely that this meeting will yield much new information for investors. However, given the influence that central bankers have on financial markets, expect the meeting to be closely watched. Key speakers at the event include Mario Draghi, Jerome Powell and Haruhiko Kuroda.

OPEC and a group of non-OPEC producers including Russia are holding a meeting in Vienna on Friday to discuss whether to increase their oil output. The Trump administration has been putting pressure on the group to increase oil production and ahead of the meeting, powerful cartel members, Saudi Arabia and Russia, have expressed a willingness to do so. However, other members of the cartel, including Iran and Iraq, oppose an increase in oil production and as OPEC needs a unanimous decision on any changes, expect a lively meeting. In any case, the extent and timing of potential production increases will likely have a material impact on the price of oil, with the price of the commodity currently trading lower ahead of the meeting.

On the data front it is a relatively quiet week with the highlight being the release of the preliminary PMI business confidence surveys for Europe, Japan and the US. The data includes the manufacturing confidence reading in Japan whilst service, manufacturing and composite readings are released for the both Europe and the US. These forward-looking surveys will provide a useful guide to the pace of economic activity within each economy, with both the US and Europe expected to record a small decline in business confidence.

In the rear view mirror of last week we saw

Central banks and politics dominated headlines last week. As widely expected, the Fed increased interest rates by another 0.25% at their monetary policy meeting. The Fed has increased interest rates by 1.75% since they started their tightening cycle in December 2015. Fed officials were also relatively upbeat about the outlook for the US economy, with growth and household spending estimates for the year revised higher and the unemployment rate expected to fall even further to 3.5% in 2019. It was also announced that the Fed Chair, Jerome Powell will now undertake press conferences following the conclusion of each monetary policy meeting from January 2019. As the Fed have only raised interest rates at meetings that included a scheduled press conference, the shift is seen as giving them more flexibility and transparency going forward. Although committee members were quick to downplay suggestions that the change will lead to a faster pace of interest rate rises going forward.

Arguably the biggest shock of the week came from the ECB monetary policy meeting. The central bank announced that it plans to extend its quantitative easing programme (QE) from September to December, and in the process halve the number of bonds they purchase on a monthly basis as part of their quantitative easing programme from €30bn to €15bn from October. This announcement was broadly expected. The real surprise from the meeting was the announcement that interest rates will remain at present levels (-0.40%) until at least the summer of 2019. This is the first time the bank has used calendar based guidance on interest rates as part of its policy framework, previously the bank had stated that interest rates would not rise until “well past” the end of their bond purchasing programme. The interest rate announcement was seen as more “dovish”, a term used to describe monetary policy that is stimulative and supportive of growth, and after the announcement, the Euro tumbled -1.89% against the US Dollar, its worst daily decline since the Brexit vote.

As has been the case since Donald Trump took up the US Presidency, geopolitics remained in the spotlight. The meeting between President Donald Trump and North Korean Leader Kim Jong-un, offered few concrete details. Both signed a declaration that North Korea would work toward the “complete denuclearisation of the Korean Peninsula” albeit with no set timetable for this to occur. Whilst in what was seen as a major concession to North Korea, President Trump agreed to stop running joint military exercises with South Korea in the region. The positive developments at the US/North Korea summit should have meant that it was a positive week for the President and his quest to win a Nobel Peace Prize.

However, later in the week the President escalated trade tensions with China by approving tariffs on $50bn of Chinese imports, with tariffs on $34bn of Chinese imports set to be implemented on July 6th and tariffs on the remaining $16bn of imports due to go to a public hearing for implementation at a later date. In response, China announced a proportional retaliation, matching the US tariffs on date and size. The news raised fears of a global trade war and equities traded lower after the announcements.

In the side view mirrors of corporate activity we notice

It was a big week for M&A news, with a US Federal Judge’s decision to approve the $85bn merger of AT&T and Time Warner likely to kick-start a wave of M&A activity within the media and telecommunications industry. The approval of the merger is a major blow to the US Department of Justice (DoJ) who had tried to block the deal on competition grounds, in particular claims that AT&T will start to charge rival distributors higher prices for Time Warner contents – which include HBO. However, the judge accepted AT&T’s argument that owning its own media company is a necessity to take on new entrants in the media industry like Netflix and Google, who have invested heavily in original content and entertainment companies for their online streaming service.

The AT&T and Time Warner deal is rare, as it combines a content distributor (AT&T) with a producer of content (Time Warner), and arguably gives other media companies the green light to follow suit with similar “vertical” mergers - where business in different parts of the supply chain combine. The announcement certainly gave Comcast the confidence that its attempt to purchase 21st Century Fox is less likely to be blocked by US competition authorities. Following the judge’s decision, Comcast bid $65bn for parts of 21st Century Fox including Fox’s film and cable network as well as its 39% stake in Sky. The offer from Comcast is likely to kick-off a bidding war with Walt Disney Co. who had previously bid $52bn for the company. Interestingly, the battle between Comcast and Walt Disney Co. does not end there as both are currently locked in a battle to acquire the 61 percent stake in Sky not owned by Fox.

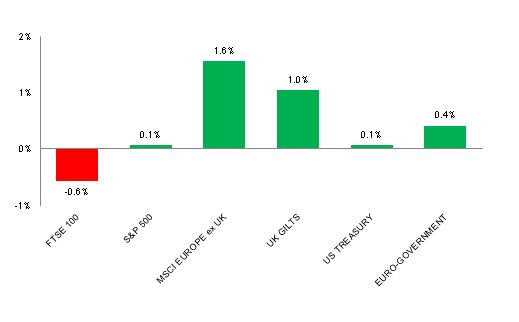

Source: Bloomberg. Figures are for the period 11th June to 17th June 2018.

Where the index is in a foreign currency, we have provided the local currency return.

The above charts provide the performance for the three developed market geographies where the TMWM MPS portfolios maintain their largest exposure. All investments and indexes can go down as well as up. Past performance is not a reliable indicator of future performance.

Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862.

Weekly View from the Front

If you are interested in receiving this communication every Monday morning, please use the button below to fill in your details.

The value of your investment can go down as well as up, and you can get back less than you originally invested. Past performance or any yields quoted should not be considered reliable indicators of future returns. Prevailing tax rates and relief are dependent on individual circumstances and are subject to change.