16th July– 22nd July 2018

Share:

- Date: 16/07/2018

Front and centre of our thoughts this week include

A busy week lies ahead, with investors kept on their toes by a host of important economic data releases, a ramp-up in US companies reporting their second quarter earnings results and some key political events.

Starting off in China, this morning economic growth numbers for the second quarter of the year were released, and showed a slight slowing in economic activity, with annual growth coming in at 6.7%, marginally down from the 6.8% recorded in the first quarter of the year. The breakdown of the figures showed retail sales were stronger-than-expected but industrial production came in below expectations.

In the UK, with the next Bank of England (BoE) Monetary Policy meeting only weeks away (2nd August), all eyes this week will be on UK economic data to determine the likelihood of rates being raised. Recent economic data has continued to show that the UK economy has regained some momentum since the slow start to the year. This week sees the release of employment data for May as well as inflation and retail sales figures for June. If these readings come in ahead of expectations, then it may be enough to convince more policymakers that the UK economy is on a relatively steady footing, and vote for an interest rate rise.

US President, Donald Trump is also due to meet Russian President, Vladimir Putin today in Helsinki. The meeting comes after the announcement on Friday that US Department of Justice, special counsel Robert Mueller, indicted 12 Russian nationals in relation to sabotaging the 2016 presidential election. The Presidents are expected to discuss Crimea and Syria, as well as sanctions against Russia, although current expectations for actions from the meeting are relatively low.

Elsewhere, US Federal Reserve Chair, Jerome Powell gives his semi-annual monetary policy testimony before Congress. We expect him to follow his recent speeches and paint the US economy in a relatively positive light. The most closely watched aspect of the speech will be Powell’s comments on trade tariffs, particularly given the recent escalation in tensions (more below), as these will help set expectations for the pace that the US Federal Reserve continues to raise rates.

The number of US companies reporting their second quarter earnings steps-up a gear this week, with 64 S&P 500 companies due to report. The list includes the remaining US banks as well as technology heavyweights Netflix and Microsoft. The results of Netflix and Microsoft in particular will be closely scrutinised as the technology sector as a whole trades on relatively expensive valuations, which are justified only by exceptional rates of future revenue growth. As a consequence, investors will be focusing on Microsoft’s ability to continue to grow revenue within their cloud service business as well as Netflix’s success at adding new subscribers in countries outside of the US, to establish whether this trend can be maintained. The results are likely to have an impact on sentiment towards the technology sector as well as equity markets on the whole.

In the rear view mirror of last week we saw

It was another week dominated by political developments, with the trade dispute between the US and China looking unlikely to be resolved anytime soon. In a significant escalation in tensions, the US Trade Representative (USTR) released a list of Chinese imports worth around $200bn that should be subject to a 10% tariff unless China changes its trade practices. The final decision on this is not expected until after a public consultation which ends on 30th August. However, if these are introduced, they would likely have a more material impact on consumer spending than the current tariffs in place. The response from Chinese officials so far has been limited, although if the tariffs are introduced, they may choose to retaliate.

The UK government also released its long-awaited Brexit White Paper, which confirmed the UK government is moving towards a “softer” Brexit. Under the proposals the UK will seek a free trade area for goods but looser trade ties on services. However, further concessions from the UK are likely to be demanded by the EU, who will likely view these proposals as “cherry picking”. EU Chief Brexit negotiator, Michel Barnier, has noted on several occasions in the past the need to protect the principles of the single market, in particular the indivisibility of the four freedoms - people, goods, services and capital.

With regards to UK economic data, the highlight was the release of the first ever monthly estimate of rolling economic growth (GDP) by the Office of National Statistics. The data remained weak but showed the UK economy has gathered some momentum as it grew by 0.2% in the three months to May, a slight improvement from the 0.0% reading in April. The figures show that the service sector continues to be the dominant driver of growth, helping to offset declines recorded in both the manufacturing and construction sectors.

In the side view mirrors of corporate activity we notice

The second quarter earnings reports for US companies started last week, and the results so far have been fairly mixed. PepsiCo reported better-than-expected earnings, which saw its share price record the biggest daily gain since the 4th August 2009, up 4.76% last Tuesday.

Whilst US banks reporting results, JP Morgan, Wells Fargo & Company and Citigroup, have in general disappointed. Only JP Morgan managed to beat estimates on revenues and profit targets. Citigroup missed on revenue targets, while Wells Fargo profits continues to be hampered by its $1 billion settlement with US regulators for overcharging customers who took out mortgage and auto loans. After the results, all banks shares ended the day lower.

It was announced that a consortium has been in discussions regarding a cash offer for John Laing Infrastructure, one of Europe’s largest listed infrastructure funds with exposure to operational PPP projects, at an approximate 19.8% premium to Friday’s closing price. This will come as good news for the listed UK infrastructure sector following a turbulent period, with talk of nationalisation and the collapse of Carillion weighing heavily on prices. Should the offer complete, this may serve as a short term catalyst for a re-rating across a sector which offers investors exposure to high quality, inflation linked cash flows.

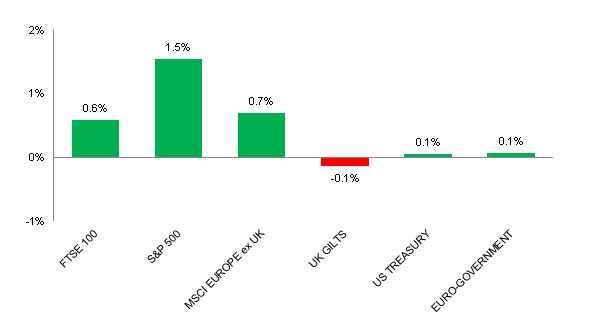

Source: Bloomberg. Figures are for the period 9th July to 15th July 2018.

Where the index is in a foreign currency, we have provided the local currency return.

The above charts provide the performance for the three developed market geographies where the TMWM MPS portfolios maintain their largest exposure. All investments and indexes can go down as well as up. Past performance is not a reliable indicator of future performance.

Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862.

Weekly View from the Front

If you are interested in receiving this communication every Monday morning, please use the button below to fill in your details.

The value of your investment can go down as well as up, and you can get back less than you originally invested. Past performance or any yields quoted should not be considered reliable indicators of future returns. Prevailing tax rates and relief are dependent on individual circumstances and are subject to change.