13th August – 19th August 2018

Share:

- Date: 13/08/2018

Front and centre of our thoughts this week include

Politics dominated news flow last week with the US escalating political tensions with China, Russia and Turkey. Investors will be keeping a close eye on how these political developments progress this week. Politics aside, it is also a busy week for economic data with a number of important data releases from the UK, US and China.

Starting with the UK, this week sees the release of retail sales and inflation figures for July as well as employment data for June. After two months of strong growth, retail sales unexpectedly declined in June with the start of the World Cup and the heatwave in the UK impacting sales. Given the persistence of the hot weather in July and England’s journey to the World cup semi-finals both factors are likely to continue to have had an influence on retail sales making it difficult to establish a trend in the data. Nevertheless, expectations are for retail sales excluding fuel to rebound in July and increase by 0.2% over the month. UK inflation has been on a steady decline since reaching a peak of 3.1% in November last year, however, we may see a reversal of this trend this week with the annualised rate of inflation expected to rise to 2.5% in July, a slight increase from the 2.4% level recorded in June.

We also receive employment data for June for the UK. Since the Brexit vote, employment data has continuously defied expectations with the number of people employed growing to 35.18m, a record high. However, despite solid job creation and the unemployment rate at its lowest level since 1975 at 4.2%, wage growth remains weak. This trend looks unlikely to reverse in June, with the unemployment rate and annualised wage growth remaining at May’s 4.2% and 2.7% respective rates.

Across the pond, investors will be keeping a close eye on industrial production, retail sales and housing starts in July to provide the first insight into how the US economy started the third quarter. The recent trend in consumer spending in the US has been strong, with retail sales recording five consecutive months of gains. Expectations are that this positive run will continue with retail sales growing 0.4% in July as the windfall from Trump’s tax cuts, solid employment growth and rising wages continue to support household spending.

In China, ever since the US introduced trade tariffs on the country, economic releases have come under the spotlight for signs of any negative effects. Chinese trade data released last week showed minimal impact thus far of the trade tariffs. This week sees the release of retail sales, industrial production and fixed asset investment data for July. Of particular interest will be the release of the retail sales numbers as the Chinese government will be hoping a strong domestic economy can help offset some of the effects of the trade tariffs on growth.

Lastly, and back to politics, the UK and EU are set to restart Brexit talks this week. The pressure on negotiators to reach an agreement has been increased by Secretary of State for International Trade, Liam Fox, recently warning that the chances of the UK leaving the EU without a deal are now “60-40”. Furthermore, the soft deadline for the UK to have a final agreement on the UK divorce from the EU and a statement on future trading relationship is fast approaching – the European Council meet on the 18th October. Therefore, developments in talks are likely to be closely watched as it feels that a lack of progression at this stage may see more businesses start to implement their hard Brexit contingency plans.

In the rear view mirror of last week we saw

Second quarter economic growth numbers were the main focus last week. Japan’s economy exceeded expectations and grew by 0.5% over the second quarter, a marked improvement from the 0.2% decline recorded in the first quarter of the year. The details of the growth numbers showed that stronger than expected consumer spending and capital investment were the main drivers of growth in Japan.

In the UK, the economy grew 0.4% over the second quarter of the year, a pick-up from the 0.2% pace over the first quarter of the year. The details showed that consumer spending remains a significant driver of growth whilst net trade was a small drag on growth. The most pleasing aspect of the growth numbers was that despite all the uncertainty created by Brexit, business investment actually rose by 0.5% over the second quarter.

In other news, the White House confirmed that the second tranche of tariffs on $16bn of annual imports from China are set to be implemented on the 23rd August. As a reminder the first tranche ($34bn) was introduced on the 6th July. China quickly responded, confirming that they will match the US tariffs by imposing a 25% tariff on $16bn worth of US imports on the same date. The market reaction to the news was fairly muted, with the focus at this point remaining on whether or not the US introduces a 25% tariff on an additional $200bn of Chinese imports later this year.

Elsewhere, it looks like the US government is taking a more aggressive stance towards Russia ahead of the US mid-term elections, announcing a new set of sanctions on the country in response to the nerve agent attack in the UK. The sanctions will prevent Russia from obtaining technologies from the US that have national security implications and are set to go into effect on the 22nd August, following a 15-day congressional notification period. The US government also introduced sanctions on Turkey in response to the jailing of an American pastor. The sanctions had a material impact on sentiment towards Russia and Turkish assets, with the Ruble and Lira falling over 7% and 20% against the US dollar over the week.

In the side view mirrors of corporate activity we notice

Elon Musk, Tesla’s CEO surprised markets last week by tweeting that he is “considering taking Tesla private at $420”, which would have valued the company at around $70bn. Tesla’s stock price at the time of the announcement was trading close to $340 and initially surged 11% on the back of the announcement. However, a lack of details on how the company was going to secure the funding to go into private ownership saw some of the enthusiasm about the deal fizzle out, with the stock ending the week up a little over 3%.

House of Fraser was pulled out of administration by Sports Direct, with the Mike Ashley owned company purchasing the struggling retailer for £90m. The purchase increases Sports Direct’s presence on the struggling UK high street as the company also owns 29.9% of Debenhams. However it’s not all good news, as employees on the House of Fraser pension scheme may not benefit from the deal due to the fact that the company entered into administration before being sold. This means the pension scheme will be passed to the Pension Protection Fund, which typically pays out less to current and future employees within the scheme.

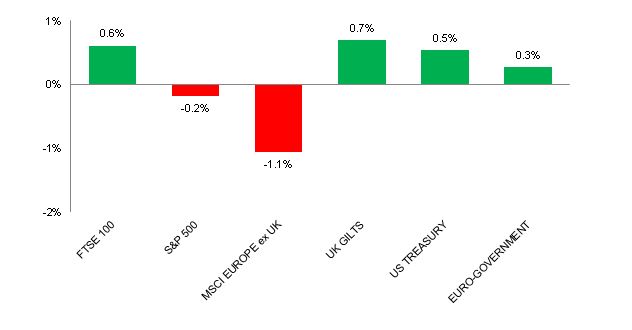

Source: Bloomberg. Figures are for the period 6th August to 10th August 2018.

Where the index is in a foreign currency, we have provided the local currency return.

The above charts provide the performance for the three developed market geographies where the TMWM MPS portfolios maintain their largest exposure. All investments and indexes can go down as well as up. Past performance is not a reliable indicator of future performance.

Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862.

Weekly View from the Front

If you are interested in receiving this communication every Monday morning, please use the button below to fill in your details.

The value of your investment can go down as well as up, and you can get back less than you originally invested. Past performance or any yields quoted should not be considered reliable indicators of future returns. Prevailing tax rates and relief are dependent on individual circumstances and are subject to change.