23rd July – 29th July 2018

Share:

- Date: 23/07/2018

Front and centre of our thoughts this week include

One of the highlights of the week will be the European Central Bank (ECB) meeting on Thursday. Although no changes are expected in terms of interest rates, it will be worth watching out for comments regarding changes going forward. What will help shape these comments is the latest Purchasing Managers Indices (PMIs) released tomorrow, which provide an insight into the health of the Eurozone economy. We get the first estimates of the manufacturing and services PMIs for July, a detailed look at how the third-quarter has kicked off for the bloc. A reminder that last month the ECB confirmed it will begin phasing out of its QE programme by year-end.

For what is a relatively quiet week in terms of economic data, plenty of attention will be on Friday when we will receive the first reading of second-quarter GDP growth for the US. Consensus for the economic growth figure is very positive, with analysts expecting a substantial acceleration from the first-quarter. After a relatively subdued annualised rate of 2.0% in the first-quarter (which was revised down from 2.2%), analysts expect growth of 4.3% in the second. One contributing factor for this sharp increase could be a boost from stronger exports as businesses attempt to front-load sales, to get ahead of impending tariffs.

Earnings season in the US is now well underway, with almost 100 of the companies in the S&P 500 having now reported earnings for the second-quarter. A further 180 US companies report this week including Alphabet, Harley-Davidson and Amazon. According to Thomson Reuters, 84% have so far reported earnings above analyst expectations, well above the long-term average of 64%. This has so far provided much-needed support to the equity index during a time when the President has been stoking up trade tensions. All this arose as US intelligence concluded that Russia did meddle in the 2016 election – despite what Trump told Putin in Helsinki last week.

As always, expect more newsflow surrounding Brexit this week. According to the FT, Prime Minister Theresa May will be sending ministers across to the EU this week to sell her Chequers Brexit plan.

In the rear view mirror of last week we saw

Last week kicked off in the US with retail sales for June, which came in roughly in line with expectations and avoided any surprises. However, the relaxed start to the week in the US did not set the tone for the rest of it, as US President Donald Trump went on to discuss various topics such as interest rates, trade and currencies.

Before going into that, we also saw Federal Reserve (Fed) chair, Jay Powell, giving a testimony to the Senate Banking Committee. This gave us the latest insight into the Fed’s view on monetary policy and, more specifically, the future path of interest rates. His statement was broadly unchanged from his previous one of confirming gradual interest rate rises, however with a new inclusion of the phrase “for now”. This still left things a little vague, as it could mean either accelerating or decelerating the rate of rises.

It’s getting tougher to keep up with President Trump’s tweets and soundbites; however the latest ones included accusing China and the EU of manipulating their currencies and interest rates lower. Despite these accusations, Trump himself last week was arguably doing this exact thing, by seemingly putting pressure on the Fed to slow, or even halt, tightening monetary policy due to worries about the strength of the dollar. Finally, it wouldn’t be a complete note regarding President Trump without mentioning escalating trade tensions – the President said on Friday last week that he was ready to impose $500bn worth of tariffs on Chinese imports.

Back in the UK, it was an important week in terms of economic data. Tuesday’s employment report for May was free from any surprises, with the unemployment rate holding at 4.2% and wage growth (average weekly earnings) at an annualised rate of 2.5%. The second important release was on Wednesday in the form of the June inflation report. Both core and headline CPI came out below expectations, with core falling below the Bank of England’s (BoE) target to 1.9% - the first time since March last year. Despite the weaker inflation, the market is still expecting the BoE to raise interest rates at their next meeting in August, with the Bloomberg-implied probability at 85%.

In the side view mirrors of corporate activity we notice

Netflix shareholders suffered last week, a rare statement, following relatively disappointing results for the second-quarter, which it described as “strong but not stellar”. Although the main focus was on the lower-than-expected subscriber growth, particularly in the US, the streaming service also missed analysts’ expectations on revenue. Shares opened down around -14%, however ended the day down a less-aggressive -5.2%. Despite this fall, the shares are still up just shy of 90% this year (trading on 131x December 2018 earnings).

Anglo-Dutch Consumer Staple giant Unilever also reported last week, with lacklustre results partly put down to a truckers strike in Brazil holding back growth. According to the FT, this strike wiped 1.2% of underlying sales growth off the second-quarter. Turnover was also hurt by currency headwinds. In addition to their trading update, it has set October 25th and 26th for Dutch and UK shareholders to vote on its proposal to abandon its dual listing.

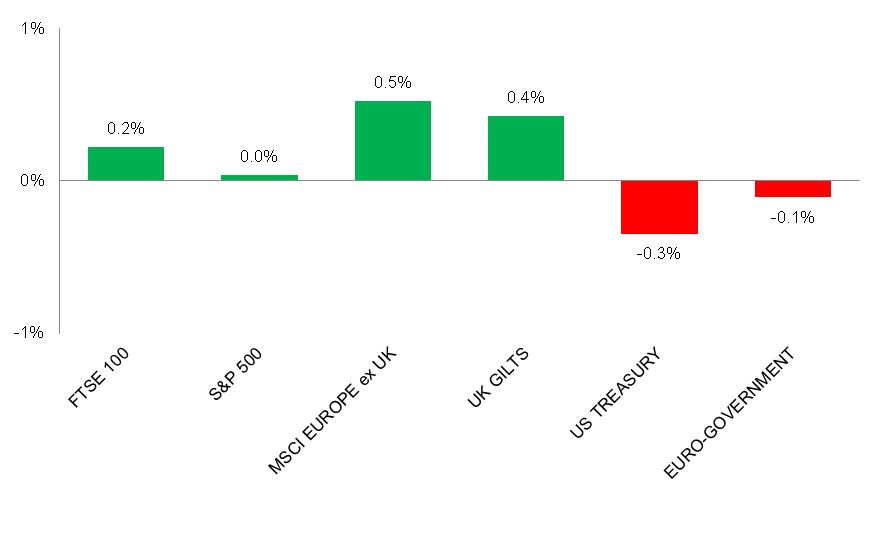

Source: Bloomberg. Figures are for the period 16th July to 22nd July 2018.

Where the index is in a foreign currency, we have provided the local currency return.

The above charts provide the performance for the three developed market geographies where the TMWM MPS portfolios maintain their largest exposure. All investments and indexes can go down as well as up. Past performance is not a reliable indicator of future performance.

Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862.

Weekly View from the Front

If you are interested in receiving this communication every Monday morning, please use the button below to fill in your details.

The value of your investment can go down as well as up, and you can get back less than you originally invested. Past performance or any yields quoted should not be considered reliable indicators of future returns. Prevailing tax rates and relief are dependent on individual circumstances and are subject to change.