6th August – 12th August 2018

Share:

- Date: 06/08/2018

Front and centre of our thoughts this week include

Following the last week’s busy schedule of economic data releases and central bank meetings, this week should be much quieter. The data highlights will virtually all fall on Friday, which will be discussed below. Today offers very little in terms of data; however it is worth noting that the US is expected to begin restoring economic sanctions on Iran today, following US President Trump pulling out of the nuclear deal in May.

Fast-forwarding to a busy Friday, we first receive Japan’s second quarter GDP growth number. A reminder that the country’s first quarter reading showed the economy contracting for the first time since 2015. Investors will be hoping for a rebound, and indeed the market consensus is for growth of +0.3% in the second quarter.

The next focus that day will then be on the UK, where we also receive the second quarter GDP figures. The annualised GDP growth for the UK has been on a gently-sloping downward trend since the end of 2014, where the growth rate peaked at 3.1%. GDP is expected to have grown 0.4% in the second quarter, which would result in the economy growing 1.3% over one year to the end of June – a slight jump from the previous 1.2%.

The latest inflation reading for the US will finish off the week’s economic data releases – we receive their July CPI report. Despite not being the Federal Reserve’s (Fed’s) main inflation metric, it will no doubt be closely watched as the market continues to monitor information that could have an impact on the Fed’s path of normalising monetary policy.

Corporate earnings season continues through this week, with 44 S&P 500 companies reporting. The bulk of the companies in the S&P 500 have now reported. Whilst there have been some high-profile misses (notably Facebook and Twitter), according to Thomson Reuters 81% of S&P 500 companies have beaten earnings expectations – if this number holds, it will be the highest percentage of beats on record.

In the rear view mirror of last week we saw

The highlight from last week saw the Bank of England (BoE) Monetary Policy Committee (MPC) members vote 9-0 in favour of raising its benchmark rate to its highest level since 2009 – to the dizzy heights of 0.75%. The pound strengthened initially off the back of the emphatic vote, before ending the day weaker than it was before the hike was announced. The reason for this was comments from the BoE governor, Mark Carney, warning on the risks of a ‘no deal’ Brexit. In terms of inflation, the minutes from the meeting showed they expect it to remain a touch ahead of the 2% target for the next couple of years.

In addition to the MPC meeting, we also received the UK’s latest purchasing managers indices (PMIs) for the manufacturing, services and construction sectors. The readings were very much mixed relative to expectations: the services PMI was well below, construction well above and manufacturing roughly in line. Mixed, but overall it seems the economy has got off to a reasonable start to the third quarter.

In a central bank-dominated week, we also had the Fed meeting on Wednesday. Fed officials voted to hang fire on raising interest rates, with the benchmark rate remaining between 1.75% and 2%.

On Friday we received the latest US jobs report for July. The unemployment rate fell to 3.9%, as expected. Wage growth has been the more anticipated release recently – this also came out in line with expectations, with an annualised growth rate of 2.7%.

The final central bank meeting to cover off was from the Bank of Japan (BoJ), which met on Monday. As expected, it voted to keep its short-term interest rate in negative territory, at -0.1%. Prior to the meeting, speculation built around the central bank making significant changes to its monetary policy, however it also maintained its 0% target for the yield on its 10-year government bond.

In the side view mirrors of corporate activity we notice

Apple reported their earnings last week, where it recorded revenue growth of 17% on an annualised basis, beating analyst estimates, with profits also jumping 32% - very impressive figures for a company their size. The iPhone X, their latest $999 model, was a key driver for the numbers, with their most popular model lifting the average selling price 20% to $724. Later in the week, the iPhone maker became the first company to reach $1 trillion in market capitalisation as the share price rallied over 9% last week.

Just over a month after the UK government sold a £2.6 billion state in RBS, the company confirmed it is to pay its first dividend since it was bailed out after the 2008/09 financial crisis. It agreed to pay an interim dividend of 2p per share, after it finalises an agreement on a fine from the US Department of Justice regarding mis-selling of mortgage-backed securities. The share price jumped about 2.5% on the day.

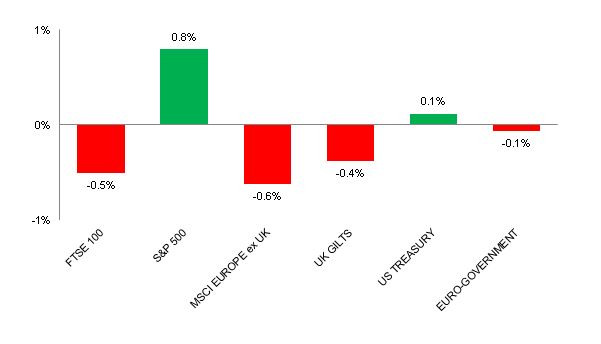

Source: Bloomberg. Figures are for the period 30th July to 3rd August 2018.

Where the index is in a foreign currency, we have provided the local currency return.

The above charts provide the performance for the three developed market geographies where the TMWM MPS portfolios maintain their largest exposure. All investments and indexes can go down as well as up. Past performance is not a reliable indicator of future performance.

Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862.

Weekly View from the Front

If you are interested in receiving this communication every Monday morning, please use the button below to fill in your details.

The value of your investment can go down as well as up, and you can get back less than you originally invested. Past performance or any yields quoted should not be considered reliable indicators of future returns. Prevailing tax rates and relief are dependent on individual circumstances and are subject to change.