How to use a trust to protect your wealth during a divorce

- Date: 11/07/2017

From ‘Baby Boomers’ to ‘Silver Splitters.’

The Baby Boomers, the children born between the end of World War 2 and the mid-1960s, have helped shape modern Britain and come through tough periods to benefit from rising property and investment values. Now this group are back in the spotlight – this time dubbed the ‘Silver Splitters’.

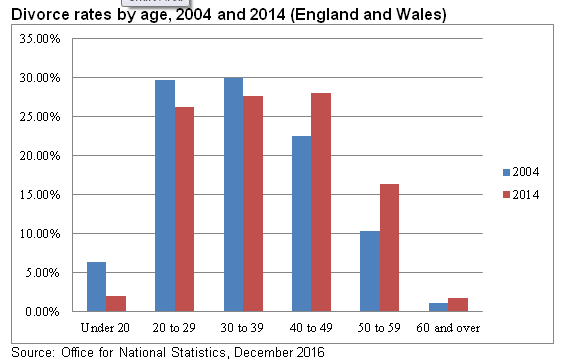

According to the Office for National Statistics, in 2004 just over 11% of divorcees were older than 50; by 2014 (the most recent survey) this figure had increased to more 18%. The number of divorcees older than 60 has also increased notably in recent years. This will be due to a number of reasons, not least that children leaving home at much later ages than previously, and a general increase in mortality, with at least one half of a couple not willing to live out their golden years in an unhappy marriage.

Click to view Graph: Divorce rates by age, 2004 and 2014 (England and Wales)

The Silver Splitters are a demographic who have largely made their money, and will often have significant assets with which to share. This is also a demographic who are likely to have children from their previous marriage and are embarking on new relationships with fellow was-Baby Boomers-now-Silver-Splitters. There is often a desire to protect assets for their children, but also to maintain stability for their new partner in the event of death.

{kind=link}

One solution to this is the Immediate Post Death Interest (IPDI) trust. The most popular reason for this arrangement is to leave a property in trust. The surviving partner has a right to live in the property, sometimes for life, or the right can be terminated if they remarry for instance. The property then passes to the children at the appropriate time.

Use of an IPDI trust also has a crucial benefit in that it allows an estate to make full use of the newly implemented Residence Nil Rate Band (RNRB) as well las provide the protection afforded by the trust structure. For married couples who die after 2020, this allows for an additional combined RNRB of £350,000 to be offset against the estate of the last surviving spouse and a potential inheritance tax saving of £140,000. This might otherwise be lost if the most common form of will trust, a discretionary trust, is used instead of a IPDI trust. Where assets are correctly arranged, IPDI trusts are also an ideal way of ensuring both RNRBs are used which might not always be the case (as the RNRB cannot be transferred between unmarried couples).

An IPDI trust fulfils the requirements for an estate to qualify for the full RNRB because the ultimate aim of the trust is to pass the main residence to a ‘direct descendant’, which accords with the controversial HMRC rules. A discretionary trust on the other hand confers no rights to a beneficiary, and therefore the RNRB cannot be claimed.

It is essential the Silver Splitters take action when divorcing, and again as new relationships are formed and children from the previous marriage are to be considered. Getting it wrong could mean that the new partner is forced to move out of their home to pay an inheritance to the deceased’s children, causing unwanted rifts, with potentially unnecessary tax implications for the families involved.

This is a very complex area and to ensure your wishes are met, there is clearly significant added value in seeking professional advice. Good advice should prevent relinquishing the ‘baby boomer’ wealth to the tax man unnecessarily.

Tom Lloyd Read, Chartered Financial Planner

Head of Advice

Article first appeared in:

What Investment (11th July 2017)

Clients are advised that the value of investments can go up as well as down.

Tax led investments can be higher risk, longer-term investments that may be difficult to sell within a reasonable timeframe and at ‘fair value’ and so will not be suitable for everyone; They should only be considered once other planning opportunities have been fully explored. The tax reliefs available to EIS and VCT investors are dependent on the companies in which you invest maintaining their qualifying status. Tax treatment depends on your individual circumstances and may be subject to change in the future.

Thomas Miller Investment is the trading name of the businesses in the Thomas Miller Investment Group. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155) and is a company registered in England, number 08284862.