Why we still have conviction in UK equity income funds despite their poor past two years’ performance

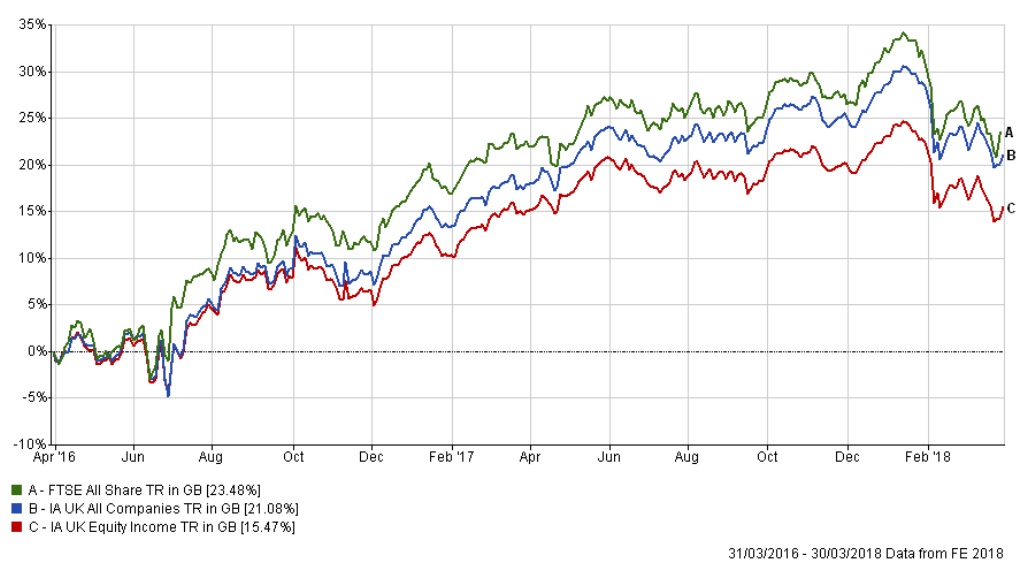

It has been a tough couple of years for active UK equity managers, a statement that won’t come as a shock and has been widely stated. However, as can be seen below, it’s UK equity income managers that have suffered the most, with the IA UK All Companies sector performing roughly in line with the FTSE All Share. This piece will be focusing on UK equity income funds and how, despite the undeniably poor past couple of years’ performance, our conviction has not waned.

At the risk of stating the obvious, it might be useful to provide our view of what an income fund is: a fund aiming to provide sustainable and growing income for investors, without simply converting capital to income.

Rather than blindly backing these managers, trusting that mean reversion will kick in and result in a period of outperformance, we’ve looked back at this period of underperformance to assess whether there are any structural issues with this form of investing. In effect, we looked firstly at the reasons for the underperformance, and secondly whether these reasons are, in our view, justifiable.

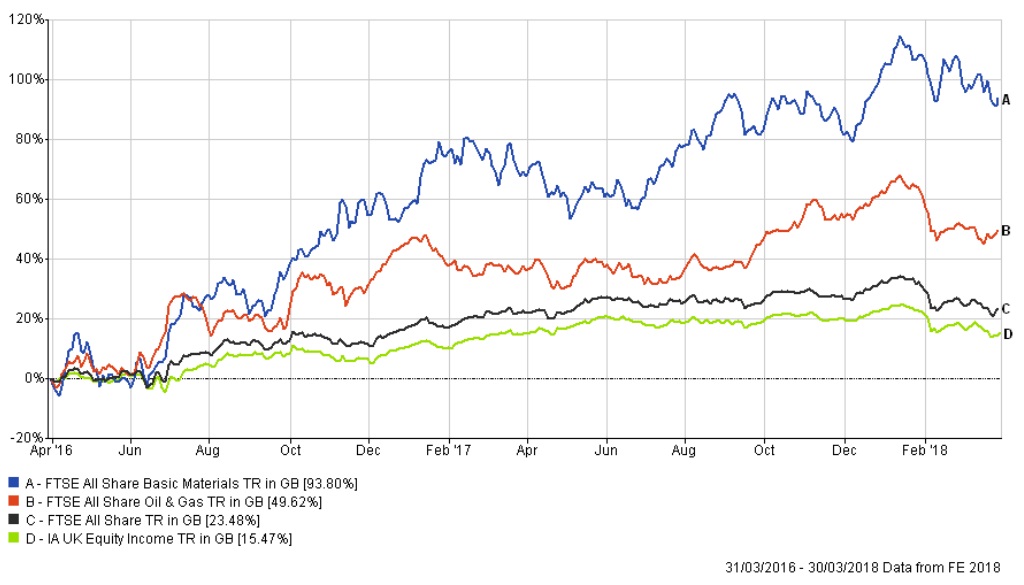

For us, the below graph is a simple snapshot that tells the majority of this underperformance story. The Basic Materials and Oil & Gas sectors have simply driven the UK market up, far and away leading the pack in terms of sector performance. To put into context, these two sectors contributed 11.8% (i.e. half) of the FTSE All Share’s returns over this period, despite the average weighting of them combined being less than a quarter of the benchmark. Put simply, if you were underweight these sectors, you would have faced a steep uphill battle to try and outperform. Indeed, the majority of the active managers in this sector were underweight these sectors.

The second key reason for the sector’s poor returns is the underperformance of domestically focused stocks. Since Britain’s EU referendum on the 23rd June 2016, these companies have de-rated and been sitting on substantial discounts relative to the wider UK market. In fact, the last time the discount was this extreme was back when the UK economy was in recession. These companies are typically at the bottom of the FTSE 100, as well as in the FTSE 250: areas of the market where these managers are overweight.

After nailing down the key reasons that contributed to this underperformance, we had a think about why the active managers have been positioned this way – is this a simple form of herding, or are they justified, leaving us comfortable with holding them going forward?

Starting with being underweight the aforementioned sectors – has this been justified? The underlying drivers of both sectors’ performance are commodity and oil prices. This results in earnings largely dependent on macro conditions which lie outside management competence and therefore could be defined as poor quality, i.e. they are not reliable or sustainable. These are highly cyclical businesses with volatile and unreliable earnings, which result in unreliable dividends. Indeed, it is not surprising to see that many firms have struggled to even cover their dividends with earnings. Royal Dutch Shell (the largest constituent in the UK equity market) has not covered its dividend since 2014, a year where the average oil price was over $90 per barrel. This may only be one company, but it can be used as a decent proxy for the wider commodity-driven sectors.

Linking back to what we look for in an income fund, sustainable dividends are paramount, and as discussed these sectors generally do not tick this box. Regarding the second criteria of avoiding capital depreciation, with hindsight it’s easy to say these equity managers were wrong over the past couple of years as not only did capital not depreciate in the sectors, it rocketed. However, you also have to take into account the amount of risk taken on our clients’ behalf. I noted above the poor quality earnings these sectors possess, with the fact that their earnings are typically out of their control and, just as importantly, very tricky (if not impossible) to accurately forecast. As a result, we actually prefer that our active managers be underweight these areas of the market, and to instead focus their attention on the higher quality, more predictable, areas – for example, companies with competitive advantages and pricing power. It may sound strange to say, but we are comfortable with our active managers under performing during periods where the market is driven up by the risky and unpredictable sectors, by sitting in the more quality, safer areas of the market. Quality as a factor has been proven to enhance returns over the long-term, but this of course means that over the short-term it may hurt relative performance.

In terms of whether these managers have made a mistake by rotating towards the more domestically focused stocks, it’s tough to tell just yet. However, it does seem as if share prices for these stocks have almost become detached from their fundamentals since the referendum. Bearing in mind most active managers’ should base their decisions on long-term fundamentals, short-term irrational behaviour in the wider market is an environment that can lead to ugly relative performance. If we do start to see some surprises to the upside for domestics’ earnings, we could well see some impressive outperformance. But, that is of course based on the big ‘if’.

What we’re trying to get across is that, although UK equity income funds have undoubtedly had a disappointing couple of years, it almost feels like it’s been a ‘perfect storm’ for them. Not only has the market been driven up by the riskier parts of the market these managers are typically underweight, but there are also indications that share prices for many underlying companies in the index have become detached from reality. We think it’s very unlikely we will see commodity and oil prices rally to the extent they have done the past couple of years (e.g. oil price over doubling), and that the worst-case scenario (and perhaps more) is built into domestics’ share prices. Both of these headwinds that UK equity income managers have faced are dissipating, and could instead turn into tailwinds. In the meantime, they have delivered on the income.

To us, there are no signs that these managers have lost their touch, or indeed that there are structural issues with this form of investing. If we stick to our long-term view, which it often feels that fewer and fewer people do, we are confident our clients will be rewarded.

Sam Buckingham

Investment Analyst

Commentary first appeared in:

Trustnet (on the 16th April 2018)

Clients are advised that the value of all investments can go up as well as down. Any past performance or yields quoted should not be considered reliable indicators of future returns. Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy.

Thomas Miller Investment is the trading name of the businesses in the Thomas Miller Investment Group. Thomas Miller Wealth Management Limited is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862. Thomas Miller Investment Ltd is authorised and regulated by the Financial Conduct Authority (Financial Services Register number 189829). It is a company registered in England, number 2187502. The registered office for both companies is 90 Fenchurch Street, London EC3M 4ST. Thomas Miller Investment (Isle of Man) Limited is licensed by the Isle of Man Financial Services Authority. It is a company registered in the Isle of Man, number 48181C. The registered office is Level 2, Samuel Harris House 5-11 St Georges Street, Douglas, Isle of Man, IM1 1AJ. Thomas Miller Investment is a registered business name of Thomas Miller Investment (Isle of Man) Limited. Telephone calls may be recorded.

- Date

- 17/04/2018