3rd September – 9th September 2018

Share:

- Date: 03/09/2018

Front and centre of our thoughts this week include

It has been a quiet couple of weeks in regards to economic data releases. However, this week sees a step-up in activity with the closely watched US employment report and global services and manufacturing sentiment surveys for August set to occupy investors’ attentions. Additionally, as politicians return from their summer recess, we expect key political battles to return to the fore with Italy in particular focus, alongside the usual culprits of Brexit and Donald Trump.

The US employment report continues to be one of the most closely followed economic indicators as it provides a good sign of the overall health of the US economy. Last month’s employment report was a little on the softer side with the US economy adding fewer jobs than expected over the month of July. Expectations are that this trend will be reversed in August with the US economy adding 194k jobs, up from the 157k created in July. The most interesting aspect of the report will be the change in average hourly wages. As the level of wage growth will help set expectations over the level of inflationary pressures within the labour market and subsequently the pace that the US Federal Reserve (Fed) tightens monetary policy.

Elsewhere, this week sees the release of the manufacturing and service sector PMI sentiment surveys for all major economies. These will be closely watched as they continue to be one of the best leading indicators of immediate economic growth. Most major economies are expected to report business optimism that is more or less in-line with last month’s readings which would suggest that global growth remains on a steady footing.

In regards to politics, the battle between Rome and the European Union (EU) looks set to intensify as the deadline for the Italian government to produce their 2019 budget draws closer – Italy has to present its annual Stability and Growth Pact to the EU on the 27th September and its budget by the 15th October. At the heart of the issue is the fact that the coalition, populist Italian government wants to implement a number of its campaign pledges, including tax cuts, the introduction of basic income and the removal of VAT increases. If introduced it would materially worsen Italy’s national debt profile but, more importantly likely breach EU fiscal rules. The situation remains delicately balanced and we expect Italian assets to be extremely volatile over the coming weeks as they move in-line with the progress of talks.

Donald Trump will remain in the limelight with the US government expected to impose more tariffs on China later this week. Mr Trump made it clear last week that he intends to impose tariffs on an additional $200bn of Chinese imports once the public consultation period ends on 6th September. A process which is likely to trigger a response from China and likely worsen sentiment towards emerging markets at an already challenging time.

Lastly, Brexit negotiations will continue to remain in focus. Talks appeared to be going in a positive direction after Michel Barnier stated last week that the EU is “prepared to offer a partnership with Britain such as has never been with any other countries”. However, optimism of a deal appeared to dampen over the weekend with Mr Barnier noting in an interview with a German newspaper he was “strictly against the British proposal” - in particular the UK’s desire to have free movement of goods but not services or people. The remarks seemed to raise the prospects of a “no deal” Brexit with the Pound slightly weaker this morning after strengthening over the past week.

In the rear view mirror of last week we saw

It was hard to ignore politics last week, and yet again it was Donald Trump in the spotlight as he continued to raise trade tensions. Europe was last week’s target, with the EU’s offer to bring down car tariffs to zero if the US reciprocates quickly dismissed by the president, who stated it was “not good enough”. Trump also repeated his threat to withdraw the US from the WTO “if they don’t shape up”. The only positive news on trade was that the US and Canada will continue in negotiations on NAFTA this week with the hope that a trilateral deal with Mexico can be agreed later this week.

It was another challenging week for Argentina and Turkey. In an effort to stem declines in the Peso, the Argentinian central bank increased interest rates to 60% from 45%, which pushed Argentina’s interest rates to the highest in the world. The Turkish Lira also came under further pressure after the Central Bank Deputy Governor Erkan Kilimci resigned, just two weeks’ before the Central Bank are set to meet again (13th September). Whilst neither Argentina nor Turkey account for a large amount of global GDP, there are growing concerns that they present contagion risks. European banks in particular have exposure to Turkey. The crisis in both countries is a result of each country having large amounts of dollar denominated debt and as both the Peso and Lira decline it makes it more difficult for both the government and corporations to repay these debts. The broader concern for investors is that Argentina and Turkey represent early examples of the challenges that the global economy faces in an environment where the US Fed withdraws liquidity and raises global interest rates. More countries could follow suit.

Whilst it was a relatively quiet week in regards to economic data, we learned that the US economy grew more than initially thought over the second quarter of 2018, with the economy growing at an annual rate of 4.2%, marginally higher than the 4.1% originally estimated. The upward revision was due to stronger than expected government spending and business investment, although disappointingly, consumer spending was revised lower. Elsewhere, the Federal Reserve’s (Fed) preferred measure of inflation, the Core PCE Index rose to 1.98% in July, putting the inflation measure just below the Fed’s 2% inflation target.

In the side view mirrors of corporate activity we notice

Whitbread, has agreed to sell Costa Coffee to Coca-Cola for £3.9bn. Whitbread had intended to spin off the business as a separate firm, but said a straight sale was more profitable, and will allow the business to focus on growing its hotel business, Premier Inn. For Coca-Cola, hot beverages was one of the few remaining segments of the beverage market that it did not have a global brand and the deal will now give the business nearly 4,000 coffee outlets across UK and Europe. The deal is expected to close in the first half of 2019, subject to shareholder and regulatory approval.

Wonga, the UK’s largest payday lender, collapsed into administration last week. The lender had received £10m in emergency funding from investors last month to stay afloat but struggled due to a surge in complaints from former customers. The company blamed the Payment Protection Insurance (PPI) scandal for a rise in complaints from professional claims management companies.

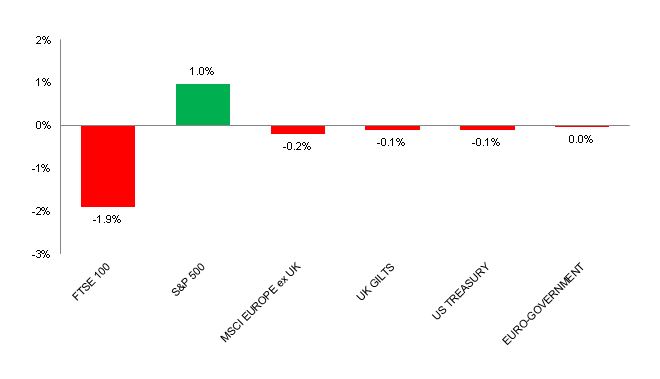

Source: Bloomberg. Figures are for the period 27th August to 31st August 2018.

Where the index is in a foreign currency, we have provided the local currency return.

The above chart provides the performance for the three developed market geographies where the TMWM MPS portfolios maintain their largest exposure. All investments and indexes can go down as well as up. Past performance is not a reliable indicator of future performance.

Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862.

Weekly View from the Front

If you are interested in receiving this communication every Monday morning, please use the button below to fill in your details.

The value of your investment can go down as well as up, and you can get back less than you originally invested. Past performance or any yields quoted should not be considered reliable indicators of future returns. Prevailing tax rates and relief are dependent on individual circumstances and are subject to change.