28th May – 3rd June 2018

Share:

- Date: 28/05/2018

Front and centre of our thoughts this week include

It may be a holiday shortened week, but it’s still a busy one in financial markets, with a number of key data releases that will help determine the pace that central banks’ tighten monetary policy.

In the US, the Federal Reserve (Fed) is widely expected to raise interest rates again at its next monetary policy meeting held over the 12-13th June – with markets currently pricing in an 80% probability of this outcome. This week sees the release of the monthly employment report (known as non-farm payrolls). A strong report showing a better than expected pace of hiring and a bigger pick-up in wages should all but guarantee a rate rise. The report is expected to show the US economy created 195k jobs in May, an increase from the 164k created in the previous month. Perhaps the most closely-watched aspect of the report will be the growth in hourly wages as these will provide an indication of the inflationary pressures within the labour market. Additionally, we also receive the core PCE measure of inflation for April, which will provide an additional guide on the price pressures within the US economy. Expectations are for core PCE to have slowed to an annual rate of 1.8%, down from the 1.9% reading in March.

In Europe, the political chaos in Italy is likely to dominate news flow. The decision by Italy’s President, Sergio Mattarella, to reject Paolo Savona, who had previously suggested Italy should leave the Euro, as finance minister has increased the risk of new elections in the country. The President’s decision led to the collapse of the Five Star Movement / League Party coalition government, with former IMF official, Carlo Cottarelli, given the tough task of trying to form a government - a result that looks increasingly unlikely as both the Five Star Movement and League are expected to vote against a Cottarelli government in parliament. If as expected, Cottarelli fails to win a vote of confidence, new elections in Italy are expected around August/September, which could increase the number of votes for both the Five Star Movement and League parties and give them a stronger mandate to defy the EU and pass an expansionary budget. Italian equities are down and bond yields rose due to the political developments.

The political situation in Italy adds another layer of uncertainty to the European Central Bank (ECB) decision on when to end their monetary stimulus (bond purchasing programme). European economic data since the start of the year has continued to disappoint, with the Citigroup Economic Surprise index for the region, which measures data relative to expectations, falling to the lowest level since 2011. This has made it harder for the ECB to justify ending is monetary programme (set to end in September). This week sees the release of May CPI inflation measure for the Euro area, which is expected to show inflation has risen to an annual rate of 1.6%. A reading below this level may cast further doubt over the ECB’s plan to end their bond purchasing programme, and investors narrative may switch, from when the ECB plans to end, to how long it plans to extend its monetary stimulus programme. However, if the Italian government breaks EU rules on budget spending, it will be difficult for the ECB to continue to purchase Italian government bonds as part of their stimulus package.

In the UK, Bank of England (BoE) housing data for March and manufacturing firms’ sentiment survey for May will be the focal points this week for investors. Housing activity in the UK has continued to slow as buyer demand has been weakened by stamp duty and tax changes as well as a slower pace of house price growth. This week sees the release of mortgage approvals for March which will provide a good indication of how well the housing market is doing as we enter the crucial spring buying season. Additionally, we also see manufacturing confidence sentiment surveys for May, which have mirrored the trend in the European sentiment surveys and been on a declining trend since the start of the year. If this trend persists and points to a further slowdown in activity, then it may cast doubt about a rebound in economic activity over the second quarter and an interest rate hike in August.

In the rear view mirror of last week we saw

It was another week where politics once again dominated headlines. Global trade tensions appeared to be easing after China announced that it will cut the import tariffs on automobiles and car parts from 25% to 15% from the 1st July. This followed the decision by both the US and China to delay imposing trade tariffs on one another while trade negotiations are on-going. However, with Donald Trump as President the situation will always remain volatile and trade tensions spiked in the latter part of the week on the US government announcement that it is opening an investigation to see whether tariffs are needed on auto and truck manufacturing industries on national security grounds - a decision that provoked an angry response from US trading partners.

In the UK, there were early signs of a rebound in economic activity after the slow start to the year. Retail sales for April were stronger than expected and provided some encouragement that the weather-related weakness in consumption over the first quarter of this year will prove temporary. Elsewhere, Consumer Price Inflation for April, rose at a lower rate than expected, 2.4% annually, and continues to trend lower and closer to the BoE’s 2% inflation target. Meanwhile the second estimate of economic growth in the first quarter of the year confirmed the initial estimate of 0.1% - the slowest pace of growth since 2012.

In the US, the minutes of the Federal Reserve (Fed) monetary policy meeting indicated that the Fed is likely to maintain its gradual pace of policy tightening and raise rates again in June. The minutes showed most policymakers agreed that if incoming data evolve as they expect another increase in interest rates would “soon be appropriate”. Data supported the case for a June rate hike. The preliminary manufacturing and service sector sentiment surveys were both above expectations and point to a solid pace of economic growth going forward - with confidence amongst manufacturers at a 44-month high.

In the Eurozone, the preliminary manufacturing and service sector confidence surveys were both below expectations and suggest a further loss in economic momentum in the region.

In the side view mirrors of corporate activity we notice

Marks and Spencer (M&S) announced a 62% decline in pre-tax profits for the financial year ending 31st March, with the retailer making a pre-tax profit of £66.8m. A considerable amount of the decline in profits was a result of costs (£321m) related to the turnaround of the business. M&S is attempting to grow its online sales whilst at the same time reduce its high street presence as consumers increasingly shift their spending on-line. As part of a five-year turnaround plan, the business announced plans to close a total of 100 stores by 2020.

Hot on the heels of the US Supreme Court’s decision to lift the ban on sports betting in most states in the US, Paddy Power Betfair announced that it has agreed to merge with the US fantasy sports betting site FanDuel. Under the terms of the deal, Paddy Power Betfair will take a 61% stake in the combined business and existing FanDuel investors will own 39%. PaddyPower stated that the deal strengthens its opportunities to target the prospective US sports betting market once states draw up their own gambling laws.

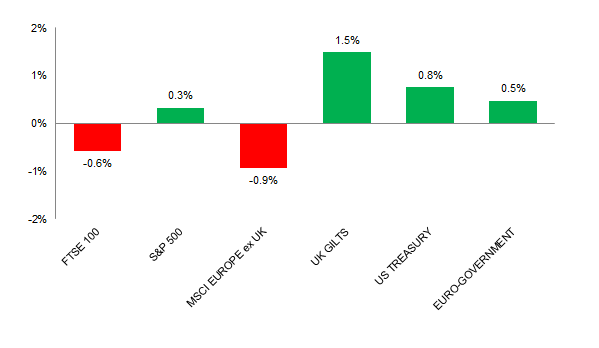

Source: Bloomberg. Figures are for the period 21st May to 27th May 2018.

Where the index is in a foreign currency, we have provided the local currency return.

The above charts provide the performance for the three developed market geographies where the TMWM MPS portfolios maintain their largest exposure. All investments and indexes can go down as well as up. Past performance is not a reliable indicator of future performance.

Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862.

Weekly View from the Front

If you are interested in receiving this communication every Monday morning, please use the button below to fill in your details.

The value of your investment can go down as well as up, and you can get back less than you originally invested. Past performance or any yields quoted should not be considered reliable indicators of future returns. Prevailing tax rates and relief are dependent on individual circumstances and are subject to change.