26th November – 2nd December 2018

Share:

- Date: 26/11/2018

Front and centre of our thoughts this week include

A fairly quiet upcoming week for global economic data, naturally the same can’t be said for global politics in the current climate. The release of the German IFO business climate index this morning confirmed an economy that appears to be weakening, whether this is temporary remains to be seen. We will be looking for more detail to assess the state of the German economy when we receive both unemployment and inflation data for November on Thursday. The unemployment rate is expected to remain steady at 5.1% while inflation is expected to tick up marginally to 2.5% (year-on-year).

There are a significant number of retail sales data released in the UK this week, some of which will provide real time sales data on Black Friday (and the now official - Cyber Monday). Over the weekend, preliminary reports have suggested that overall Black Friday sales were down in the UK this year. On Tuesday we’ll receive November CBI retail sales data, while the following day will see the November BRC shop price index released which will provide a view on how much pricing power retailers currently have.

The US provides the majority of this week’s data highlights, including the second estimate of GDP for the third quarter. The second quarter grew at a particularly strong rate of 4.2% and we expect this to be the high point for 2018. The first estimate for Q3, released earlier this month, recorded economic growth at 3.5% which is still above the potential trend rate.

The personal consumption expenditures (PCE) index is the Federal Reserve’s preferred measure of inflation and is released on Thursday. This is timely because the Fed later release the minutes from their most recent monetary policy meeting which took place in early November. Jerome Powell also gives a speech on “The Federal Reserve’s Framework for Monitoring Financial Stability” on Wednesday. Investors will be keeping a close eye on this for clues on whether next month’s widely anticipated interest rate rise is a formality or not.

As we approach the end of the week the eyes of the world will shift to Buenos Aires where the two-day G20 Leaders Summit will take place. In reality this meeting simply provides the backdrop to the ‘side meeting’ being held by US President Donald Trump and Chinese President Xi Jingping where the two leaders are expected to discuss the ongoing trade tensions. The communique is still being negotiated and continues to be a key source of contention. This is consistent with the friction that was experienced at last year’s G20 in Germany and then again at the G7 in Canada earlier this year when President Trump left the summit early.

Going on in the engine of Brexit

The weekend news saw the EU Leaders Summit pass without any controversy on Sunday night with the withdrawal agreement being signed off. We have noted previously on the blog that we didn’t envisage this part being the most difficult, as this deal now needs to be ratified by Parliament. With the Conservative Party so highly splintered, the opposition party with no clear view on the deal and the DUP against it, the outcome remains binary. With just over four months until the UK is scheduled to leave the EU on the 29th March 2019, MPs will need to work hard to come to a solution.

Today sees Prime Minister Theresa May embark on a two week campaign to sell the withdrawal agreement. The House of Commons vote is pencilled in for December 12th yet some commentators are looking beyond this as many expect the PM to fail to win the backing for her deal at the first attempt. However, it is still not clear what options are left should the deal be eventually blocked – European leaders last night were quick to point out that there were no better deals on offer.

In the rear view mirror of last week we saw

It was another weak period for equity markets last week, despite a brief rally mid-week. Market volumes were lower later in the week as the US celebrated Thanksgiving but in any case the economic data broadly pointed to a softening in macro momentum.

This is increasingly apparent in Europe where the preliminary November PMI data revealed the composite for the Euro area (i.e. both services and manufacturing industries) has ticked lower again (at 52.4) and is approaching the ’50-mark’. If it dropped below this number it would be considered a recessionary signal. This is all extremely important in the context of monetary policy for the European bloc where the ECB meet on December 13th and have widely flagged an end to Eurozone “QE”. Throw in the recent deterioration in relations with the new Italian government and there may still be more drama for Europe’s monetary policy makers.

Orders for durable goods garnered the most attention last week as they fell 4.4% in October from the previous month, the biggest monthly fall since July of last year. Whilst this reflected a sharp drop in the volatile aircraft category, even when accounting for this the reading was still soft. The overall weakness in this data suggests that the slower pace of economic growth in the third quarter is feeding into the final quarter of the year. Oil prices again fell heavily last week, with Brent trading below $60 per barrel from a high in October of $86.

In the side view mirrors of corporate activity we notice

The UK healthcare sector continues to be swallowed up by their US peers as medical devices company Boston Scientific acquired BTG, a UK healthcare company that generates therapies and specialty pharmaceuticals. BTG was created in 1981 by the merger of the National Research & Development Council and the National Enterprise Board.

The big news last week was the dismissal of Nissan chief Carlos Ghosn who was arrested for misleading investors about the size of his salary and misusing company assets for personal gain. Mr Ghosn had, previously, skilfully turned around the fortunes of Nissan, Renault and Mitsubishi in a three-carmaker alliance that allowed the company to grow significantly. His dismissal sent the share price tumbling.

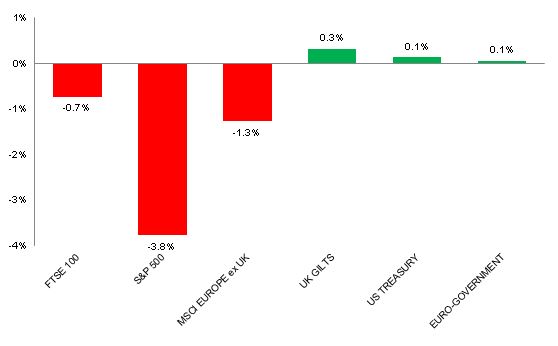

Source: Bloomberg. Figures are for the period 19th November to 23rd November 2018.

Where the index is in a foreign currency, we have provided the local currency return.

The above chart provides the performance for the three developed market geographies where the TMWM MPS portfolios maintain their largest exposure. All investments and indexes can go down as well as up. Past performance is not a reliable indicator of future performance.

Opinions, interpretations and conclusions expressed in this document represent our judgement as of this date and are subject to change. Furthermore, the content is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or a solicitation to buy or sell any securities or to adopt any investment strategy. This note has been issued by Thomas Miller Wealth Management Limited which is authorised and regulated by the Financial Conduct Authority (Financial Services Register Number 594155). It is a company registered in England, number 08284862.

Weekly View from the Front

If you are interested in receiving this communication every Monday morning, please use the button below to fill in your details.

The value of your investment can go down as well as up, and you can get back less than you originally invested. Past performance or any yields quoted should not be considered reliable indicators of future returns. Prevailing tax rates and relief are dependent on individual circumstances and are subject to change.